![]()

Advertiser Disclosure

Last update: June 11, 2025

12 minutes read

10 Credit Cards That Can Help You Build Credit with Bad Credit

Find the best no-annual-fee credit cards for bad credit. Compare secured and unsecured options, get approval tips, and start rebuilding your score today.

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

In today’s financial landscape, having bad credit can feel like an obstacle that limits your access to essential finance tools like credit cards for bad credit. However, selecting the right credit cards for rebuilding credit can put you on a path to recovery.

With the right strategy—combining responsible use of credit builder cards for bad credit, strategic choices, and a clear understanding of card features—you can steadily improve your score. This guide lays out the top criteria to evaluate before you hit “apply.”

Key takeaways

- Choosing the right credit card is crucial for building credit with bad credit

- Responsible financial habits pave the way for improved credit scores and financial opportunities

- Secured credit cards usually provide a good starting point for people looking to rebuild their credit

What is credit building, and why does it matter?

Credit building is an essential financial activity that involves improving your credit score through responsible credit usage. For people with bad credit, it's an opportunity to start fresh, correcting past financial mistakes to prove their reliability as borrowers to lenders.

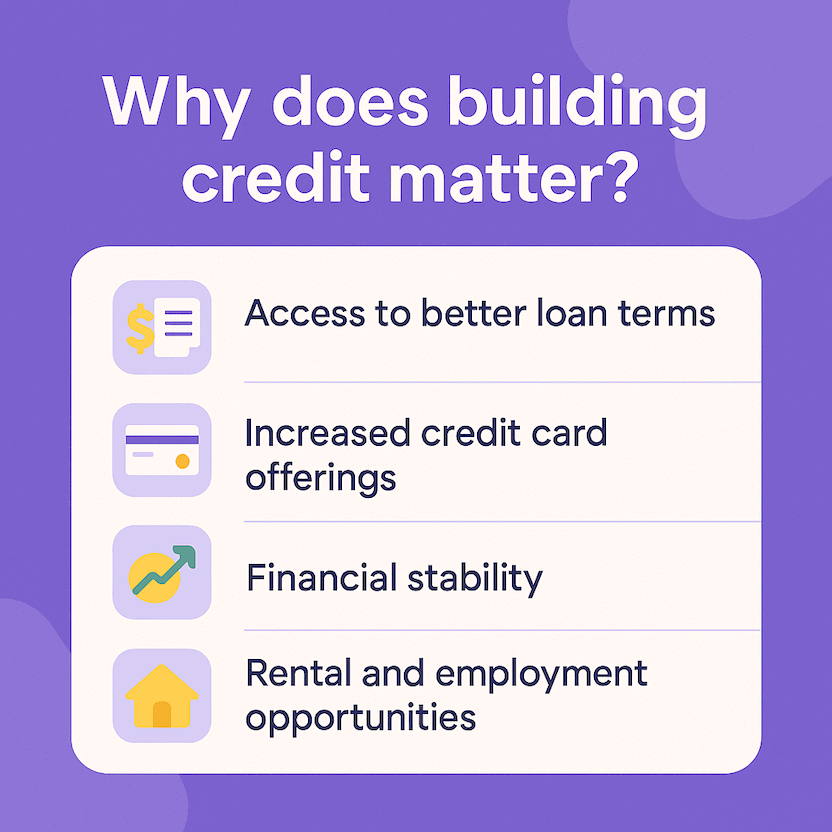

Why do people care about building their credit? There are plenty of reasons:

- Access to better loan terms: Improved credit scores usually lead to lower interest rates and better loan terms, saving money over time.

- Increased credit card offerings: Higher credit scores unlock access to credit cards with more attractive rewards and benefits.

- Financial stability: Building credit improves financial security by ensuring access to funds in case of emergencies.

- Rental and employment opportunities: Many landlords and employers check credit history as part of the hiring process, especially for positions that require financial responsibility.

How do these credit cards help you build credit with bad credit?

Building credit when you have bad credit might feel like a catch-22 situation. Features like low APR and reduced fees make building credit easier, but they’re also hard to qualify for if you don’t already have good credit.

Thankfully, it’s still possible to qualify for cards that can help you rebuild your credit - you just need to know where to look and how to use them.

With disciplined use—like making purchases you can afford, paying the balance in full each month, and always paying on time—you can gradually improve your credit score. Here, we explore ten credit cards that can help you rebuild your credit, highlighting their unique features, benefits, and drawbacks.

1. Capital One Platinum Secured Credit Card

The Capital One Platinum Secured Credit Card is a great starting point for people looking to improve their credit. Offering the possibility to qualify for a higher credit line after making your first six monthly payments on time motivates consistent, responsible credit behavior.

Pros

- Low initial security deposit options

- Automatic consideration for a higher credit line

- Reports to all three major credit bureaus

Cons

- Requires a security deposit

- No rewards program

2. Discover it® Secured Credit Card

One of the few secured cards offering cashback rewards, the Discover it® Secured Credit Card provides an incentive to spend wisely and pay off balances while giving you the chance to build credit.

Pros

- 1-2% cashback rewards on every purchase

- Automatic account review for upgrade to an unsecured card

- No annual fee

Cons

- Security deposit required

- Higher APR compared to some cards

3. OpenSky® Secured Visa® Credit Card

The OpenSky® Secured Visa® Credit Card is unique because it doesn't require a credit check or a bank account, making it accessible to many applicants looking to improve their credit scores.

Pros

- No credit check is required for application

- Can pay deposit and bills with a money order or Western Union

- Reports to all three credit bureaus

Cons

- Annual fee

- Security deposit does not earn interest

4. AvantCard

The AvantCard is tailored for people with bad to fair credit. It offers a straightforward opportunity to build credit with responsible use, thanks to its reporting to the major credit bureaus despite having a higher APR.

Pros

- No deposit required

- Reports to the major credit bureaus

- Quick and easy application process

Cons

- High APR

- $19-$99 Annual fee after the first year

5. Credit One Bank® Secured Card

The Credit One Bank® Secured Card is another solid option for people looking to build credit, offering 1% cash back on eligible purchases and the possibility of an automatic review for credit line increases.

Pros

- 1% cash back on eligible purchases

- No annual fee

- Security deposit earns interest

Cons

- Requires a security deposit

- Limited reward categories

TuitionHero Tip

Each credit card offers a path to better credit when used wisely.

6. Credit One Bank American Express® Card for Rebuilding Credit

Combining the prestige of American Express with the functional need to rebuild credit, this card offers rewards alongside credit-building opportunities, albeit with fees involved.

Pros

- 1% cash back on all purchases

- Access to American Express offers

- Reports to three major credit bureaus

Cons

- $39 Annual fee

- High APR after the first year

7. Capital One Quicksilver Secured Cash Rewards Credit Card

For people who want to keep earning rewards while building credit, the Capital One Quicksilver Secured Cash Rewards Credit Card gives you cashback on purchases and a path to an unsecured card.

Pros

- Cash back rewards on every purchase

- No annual fee

- Consideration for a higher credit limit

Cons

- Requires a security deposit

- Variable APR

8. Platinum Prestige Mastercard® Secured Credit Card (by First Progress)

With its relatively low APR and cashback rewards, the Platinum Prestige Mastercard® Secured Credit Card stands out among secured cards, offering a more affordable path to credit building.

Pros

- Low ongoing APR

- Cash back rewards program

- Reports to all three credit bureaus

Cons

- $49 annual fee

- Requires a security deposit

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

9. Chime Secured Card

One of the newer players in the space, the Chime secured card is a great choice as it comes with no annual fees, no credit check, and no minimum security deposit. It’s a choose-your-own-adventure for building credit.

Pros

- No minimum security deposit required

- Quick and easy application process

- No credit check

- No annual fee

Cons

- Requires a Chime checking account with a $200 monthly direct deposit to qualify

- No cashback or rewards

10. Mission Lane Visa® Credit Card

The Mission Lane card caters to people with not-so-great credit by offering an unsecured line of credit, which means no security deposit, but you should carefully consider its terms.

Pros

- No security deposit required

- Reports to major credit bureaus

- No annual fee

Cons

- Not everyone will qualify

- High APR

By understanding the pros and cons, you can choose the card that best suits your financial situation and goals, setting the stage for a brighter financial future.

Key criteria for choosing a card when you have bad credit

Whether you’re browsing credit-building credit cards for bad credit or looking at credit cards to help rebuild credit, run every offer through these filters to avoid surprises and maximize your odds:

- Pre-qualification & soft pull tools: Look for issuers that offer a soft credit check preview. This lets you see probable APR, fees, and credit limits without dinging your score. If you get approved there, your hard inquiry is far less risky.

- Deposit flexibility: Some secured cards (e.g. Capital One Platinum Secured) let you build up your deposit in installments. Others link to a savings account instead of a lump-sum deposit. Flexible deposit options can be a lifesaver if you’re budgeting tightly.

- Reporting to all three bureaus: Confirm in writing that your issuer reports to Equifax, Experian, and TransUnion every month. If they skip one credit bureau, you’ll miss out on full credit-score benefits.

- Upgrade path & refundable deposit: Only choose secured cards with a clear path to an unsecured product—and a guarantee that your deposit is fully refundable once you graduate. That way, you keep your credit history intact and get your cash back.

- APR & fee thresholds: For unsecured rebuilder cards, aim for APRs under 30% and annual fees under $50. If you can’t qualify, consider a secured card with no annual fee instead.

Dos and don'ts of credit building

As with any effort, there are effective strategies and common pitfalls in the credit-building process. Here's a concise guide to the do’s and don'ts:

Do

Make payments on time, every time.

Keep credit utilization low.

Check credit reports regularly for errors.

Use a mix of credit types responsibly.

Consider becoming an authorized user on another person’s card.

Don't

Miss payments or pay late.

Max out your credit cards.

Ignore your credit report and the opportunity to correct errors.

Open multiple accounts in a short period.

Close old credit accounts that contribute to your credit history.

More credit-building tips

Improving your credit score requires more than just responsible credit card use. Here are some supplementary strategies that can boost your efforts:

- Explore credit-builder loans: These loans, offered by many credit unions and community banks, are designed specifically for building credit.

- Explore credit-building debit cards: There are new companies, like Fizz and Extra, offering debit cards with automatic credit-building functionality.

- Leverage tools like Experian Boost: Services like Experian Boost allow you to add utility and cell phone payments to your credit history, potentially increasing your score. Other paid services report recurring expenses, like Grow Credit and Stellarfi.

- Set up automatic payments: Automating your payments can ensure you never miss a due date, which is crucial for credit building.

- Regularly review your budget: A budget that aligns with your income and expenses can keep your spending in check, making it easier to manage credit utilization.

- Stay informed: Keep up-to-date on changes in credit reporting and scoring models, as these can affect your credit.

By adding these tips to your credit-building strategy, you'll not only improve your credit score but also enhance your overall financial health.

Advantages and disadvantages of building credit with bad credit

Building credit, especially from a position of bad credit, comes with both opportunities and challenges. It’s an essential process that can affect your future financial freedom and flexibility. Understanding the pros and cons associated with this journey can help you navigate the path more effectively.

- Improved loan and credit card approval rates

- Access to better interest rates and saving opportunities

- Enhanced credibility with landlords and employers

- Opportunities for rewards and cashback through credit-building credit cards

- Increased financial security and emergency resource access

- Requires disciplined financial management and spending restraint

- Potentially high interest rates and fees on initial credit offerings

- Security deposits for secured credit cards can tie up funds

- The risk of falling into debt if not managed properly

- It may take time to see notable improvements in credit scores

Regulatory rollbacks at the CFPB

As of May 13, 2025, the Consumer Financial Protection Bureau proposed eliminating its “bad actor” registry—a public database created in June 2024 to track nonbank firms that repeatedly violate consumer-protection laws.

It argues in its Federal Register notice that the compliance costs may outweigh unclear benefits for consumers.

In a related move on May 15, 2025, the Trump administration's CFPB quietly withdrew its December 2024 proposal to regulate data brokers under the Fair Credit Reporting Act, removing a key guardrail intended to limit the sale of Americans’ sensitive personal information without consent.

Why trust TuitionHero

TuitionHero understands how hard it is for students and parents to manage college finances. We offer tools and support for student loans, FAFSA, and credit cards. Our platform connects you with trusted lenders and tailored deals. Let us help your family make wise financial decisions and confidently build credit.

Frequently asked questions (FAQ)

To maintain a good credit utilization rate, aim to keep your credit card balance below 30% of your credit limit. This demonstrates responsible credit use and can positively affect your credit score. For instance, if your credit limit is $500, try to keep your balance below $150 at any time.

The time it takes to see improvements in your credit score can vary depending on several factors, including how consistently you make payments on time, maintain a low credit utilization rate, and responsibly manage your credit. Typically, you may start noticing positive changes within three to six months of responsible credit card use.

Yes, some credit cards for bad credit, like the AvantCard and Mission Lane Visa® Credit Card, don't require a security deposit. These unsecured cards are available to individuals with less-than-perfect credit, but they may come with higher APRs and fees.

When selecting a credit card for building credit, consider factors like the annual fee, APR, rewards program, and whether the card reports to all three major credit bureaus. Additionally, look at the card’s terms, such as security deposit requirements for secured cards or potential for credit line increases.

Yes, many secured credit cards offer a pathway to an unsecured card. For example, the Discover it® Secured Credit Card automatically reviews your account and can transition you to an unsecured card if you demonstrate responsible credit behavior over time.

High APR on credit-building cards can lead to significant interest charges if you carry a balance. It's crucial to pay off your balance in full each month to avoid these charges, especially if the card has a high APR. Doing so also helps improve your credit score by demonstrating responsible credit use.

Credit-builder loans are another tool for building credit. Unlike credit cards, these loans are typically installment loans, where you make fixed payments over time. Both can help improve your credit score, but credit-builder loans are often used by individuals who prefer not to use credit cards or want to diversify their credit profile.

Yes, alternatives to credit cards for building credit include credit-builder loans, becoming an authorized user on someone else's card, and using services like Experian Boost, which can add utility and phone payments to your credit history. Additionally, some new debit card products, like those from Fizz and Extra, offer credit-building features.

Very rarely. Introductory 0% APR offers almost always require a good to excellent credit score (typically 670+). If your credit is in “bad” territory (<630), issuers view you as higher risk and won’t extend an interest-free period.

Your best bet is to focus first on a secured card that reports to all three bureaus, build six months of perfect on-time payments, then graduate to an unsecured card that may carry a promotional APR.

Yes. On both secured and some unsecured “starter” cards, $500 is common:

- Secured cards: Simply deposit $500 and that becomes your starting limit.

- Unsecured rebuilders: Cards like the Capital One Platinum Secured or certain “bad-credit” Visa/Mastercard products often start around $300–$500 once approved.

If you begin closer to $200, you can often ask for a raise to $500 after 6–12 months of flawless payments.

Final thoughts

Choosing the right card when you have bad credit doesn’t have to be overwhelming—empower yourself with the criteria above and you’ll avoid costly surprises when selecting the best credit cards for rebuilding bad credit.

By leveraging pre-approval tools, flexible deposit options, and clear reporting pathways, you’ll be well on your way to rebuilding your credit using credit cards to rebuild credit that fit your needs.

Remember to pay on time, keep balances low, and monitor your progress through all three bureaus—never slip into behaviors that can further damage your score, like revolving debt on credit cards to build bad credit.

Whether you’re applying for a credit card for low credit or exploring credit cards with bad credit, stay disciplined and watch your score climb.

Source

- Platinum Secured Credit Card from Capital One

- Discover Secured Credit Card | Build Your Credit History

- OpenSky

- Avant Credit Card | Apply Online & Get a Decision Fast

- Credit One Bank Secured Card

- Credit One Bank American Express ® Card Perfect For Elevating Your Everyday Experiences

- Quicksilver Secured from Capital One - Credit Cards

- First Progress Credit Cards - Mastercard

- Secured Credit Building Credit Cards | Chime

Author

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

Editor

Rachel Lauren

Rachel Lauren is the co-founder and COO of Debbie, a tech startup that offers an app to help people pay off their credit card debt for good through rewards and behavioral psychology. She was previously a venture capital investor at BDMI, as well as an equity research analyst at Credit Suisse.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

4 minutes read

How to Build Credit as a Student in 2025

Wondering how to build credit as a student in 2025? Discover expert tricks to kickstart your score with cards, loans, and smart habits. Set yourself up for success now!

Learn More

6 minutes read

How to Get Your First Credit Card

Are you ready to navigate the journey of getting your first credit card? Learn the essentials step by step to avoid common pitfalls.

Learn More

6 minutes read

What is a Balance Transfer? How to Lower Credit Card Debt in 2024

Learn about balance transfers to slash debt and boost savings. Discover how to consolidate debt, save money on interest, and take control of your finances today!

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates